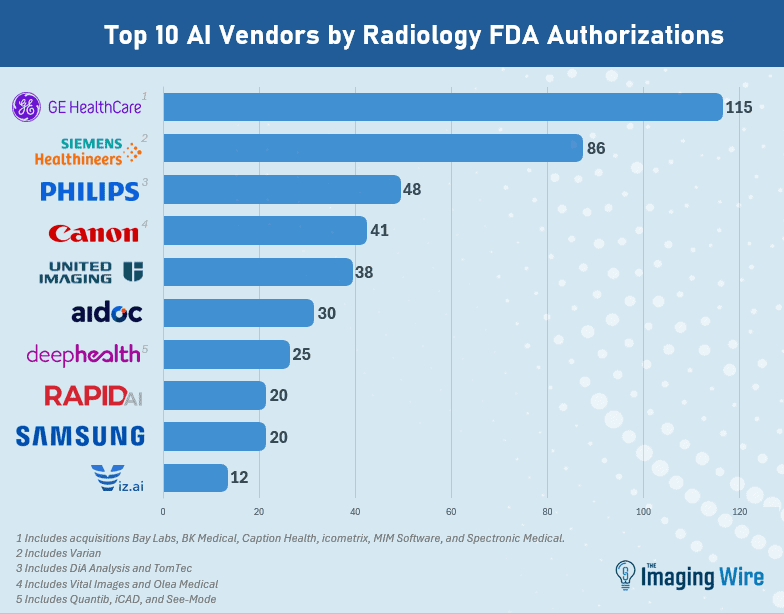

As radiology AI slowly moves from pilot projects to widespread clinical adoption, a new survey reveals a paradox: The technology is popular with radiologists, but few imaging facilities using AI have collected hard data showing its return on investment.

AI’s slow clinical adoption has frustrated both clinicians and algorithm developers alike, but the technology is gaining steam.

- Despite growing clinical evidence, research on AI’s financial value and ROI has been slower in coming.

To remedy that situation, AI governance startup Croviz.ai conducted a study of 445 radiology AI users on the economics and evaluation of AI. The full report is available here.

- Survey respondents came from 12 different countries and included a variety of professional roles, including vendor executives, radiologists, and IT and informatics personnel.

Croviz founders Ayman Talkani and AadilMehdi Sanchawala found that while radiology AI power users loved the technology – and some refused to work without it – few had determined a positive financial return from it. Findings included…

- 95% of sites already using AI had renewed at least one contract with an AI vendor in the last 12 months.

- But only 30% had quantified a positive financial ROI from AI.

- 54% cited better quality of life for radiologists as their main reason for renewing an AI contract.

So if AI’s value hasn’t been demonstrated, why are radiology sites renewing AI contracts?

- The number one reason cited by 54% of those renewing contracts was because their radiologists felt AI improved their quality of life – the only outcome measure leadership could quickly measure with qualitative user feedback.

- Lower on the scale was reduced turnaround time (18%), more scans per reader (10%), reduced downstream patient costs (10%), and better diagnostic accuracy (8%).

- Just 6% paid attention to hard metrics like staff retention rates.

What’s the best way out of the AI ROI paradox? The Croviz researchers recommended more frequent and transparent AI governance.

- Survey respondents who monitored AI performance more closely – such as more often than once per quarter – exhibited more trust in AI.

The Takeaway

The new survey offers an intriguing look at AI adoption and the question of ROI for the technology. It suggests that – much like another digital technology, PACS – AI adoption is being driven more by its popularity among radiologists than hard ROI considerations.